2021 Holiday Retail Report: Santa Came Early This Year for Retailers

-

November 19, 2021

Downloads Download Report

Download Report

-

Whether the upcoming holiday season turns out to be dazzling or disappointing, most large retailers have little to complain about this year with respect to sales. Despite economic hardships inflicted on many Americans at some point during the COVID-19 episode, the retail sector benefitted hugely once the sheer panic phase of the pandemic passed by mid-2020.

Christmas came in March this year for most consumers and retailers when the American Rescue Plan (ARP) pumped a third round of financial stimulus —some $400 billion— into the hands of most households at a time when the U.S. economy was already well on its way to recovery. This last round of stimulus was the largest and was a sizeable windfall for most recipients, many of whom were not financially impacted by the pandemic. About 80%-85% of taxpayers were eligible for stimulus payments under the ARP. This year alone, a qualifying family of four has received $8,000 of direct stimulus payments, and much of this stimulus money was quickly spent by recipients. (More on that later in our consumer survey.) This final round of stimulus under ARP, combined with a smaller stimulus package paid out in January (the Consolidated Appropriations Act), generous unemployment benefits paid through early September, a boosted and prepaid Child Care Credit and a steady recall of furloughed workers and new jobs growth since mid-to-late 2020 created ideal conditions for a consumer spending spree in 2021—and spend they have.

What we now understand more clearly in retrospect is that the COVID-induced recession of 2020 was a short but nasty affair. The U.S. retail sector experienced two dreadful months in March and April 2020 when the pandemic first hit, followed by 16 months of consistently strong sales growth, arguably unprecedented, that continues to this day. Unfortunately, smaller local businesses have suffered disproportionately during the pandemic’s surges while large omnichannel retailers have been mostly insulated from the COVID fallout or have benefitted from it.

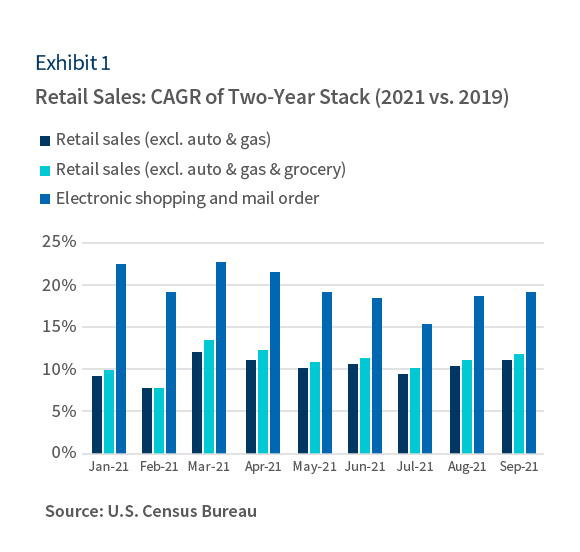

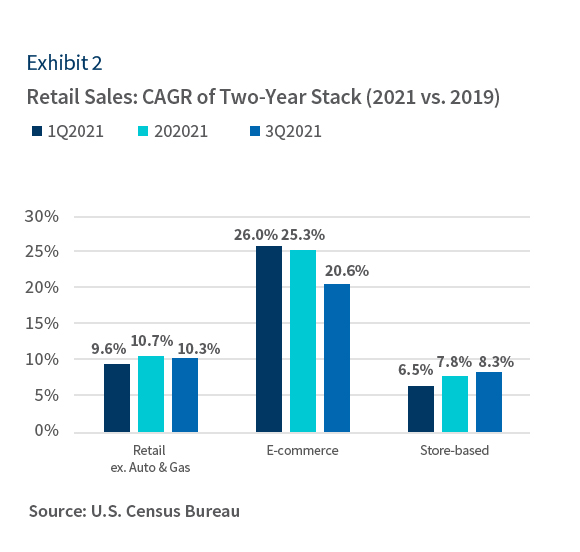

We emphasize that retail sales strength across broad categories in recent months is not the result of easy comparisons to prior year figures—as we said, sales in the second half of 2020 were surprisingly strong, including the 2020 holiday season which saw an 8.5% jump in sales over 2019. If we evaluate retail sales on a two-year stack (2021 vs. 2019, expressed as a compounded annual growth rate (CAGR)), nominal growth in the broadest retail aggregates has consistently shown a CAGR of 10% or better throughout 2021 (Exhibits 1 and 2)—the first time we can recall double-digit sales growth for such a prolonged period.

The upcoming holiday season pits consumers who are willing and able to continue spending freely against recent headwinds of waning stimulus impact, rising inflation and supply chain bottlenecks impacting retailers’ ability to keep shelves stocked and prices in check. Despite these headwinds, most forecasts are decidedly upbeat on the prospects for this holiday season, with retail sales gains mostly expected to be in high single-digit-to-low double-digit range which, if realized, would be highly consistent with sales gains in recent months, and would produce the strongest back-to-back holiday seasons on record.

Consumers are widely divided in their spending plans for this holiday season, and relatively few intend to splurge this year, as inflation and supply chain concerns are top of mind. We recently surveyed 600 consumers who spent at least $500 on holiday shopping in 2020, and their responses reflect a wide range of spending intentions.

A plurality of consumers intend to reduce their spending this holiday season.

- Despite a strong economic recovery in 2021, 38% of respondents said they intend to spend less this holiday season than last year while another 32% plan to spend the same, with only 30% indicating they would spend slightly more (18%) or significantly more (12%) than last year.

- Spending intentions varied notably among income groups, with 48% of lower income respondents planning to spend less compared to 35% for the higher income group.

- While these responses may seem inconsistent with wide expectations of a strong holiday season, higher income cohorts account for a disproportionately large share of total spending, giving their spending intentions more weight than other income groups.

Supply chain issues will weigh on holiday spending.

- Nearly 40% of respondents said they would cut back on gift purchases if supply chain issues had a detrimental effect on product availability or prices this holiday season.

- Lower income respondents were more likely to cut back on holiday spending (47%) under this scenario than the higher income group (35%).

A majority of consumers say rising inflation is impacting their shopping decisions.

- Fifty-one percent of respondents said they have experienced rising inflation recently and it has impacted their shopping decisions or behaviors.

- Thirty-one percent said rising inflation was minor or manageable, and 11% hadn’t noticed much inflation of late other than energy prices.

- Just 7% of respondents said they had not seen any notable pickup in inflation in recent months.

In-Store Shopping Bounces Back in 2021: Respite or Reversal?

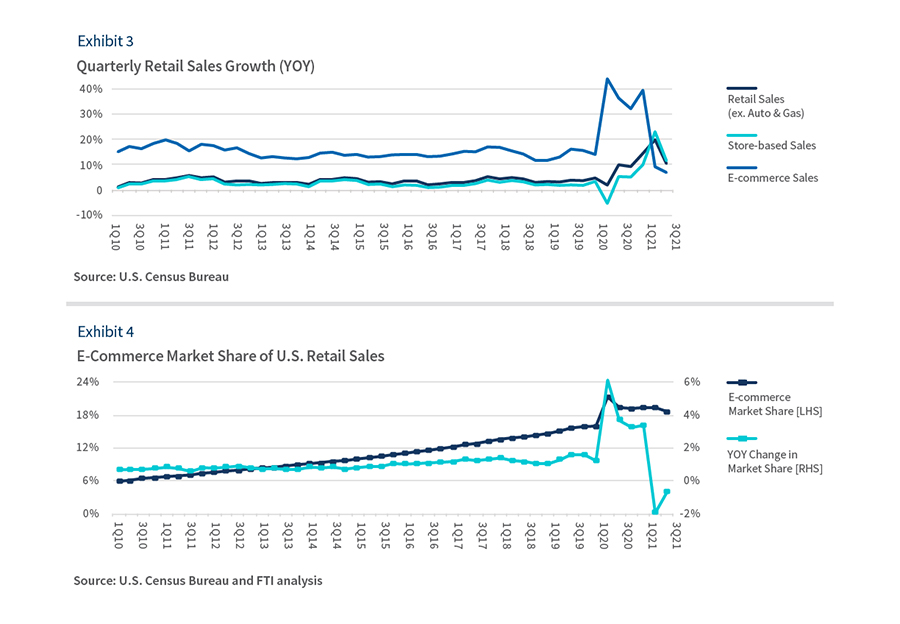

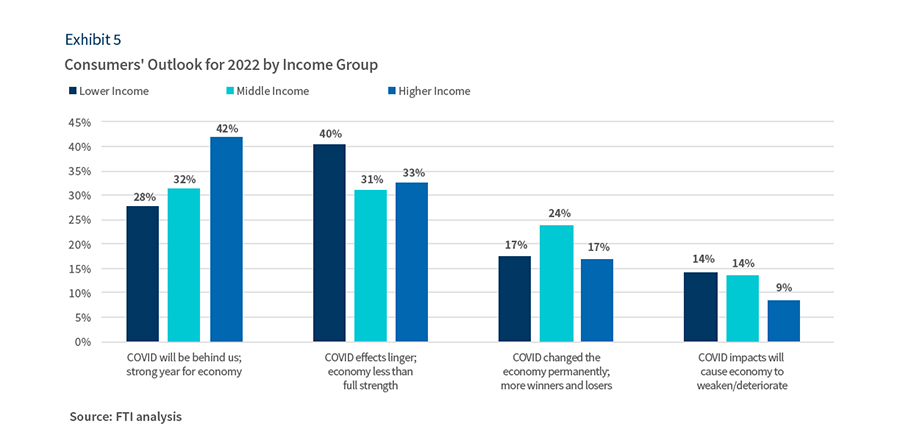

Another dynamic is playing out in the retail sector — e-commerce sales growth (YOY) has slowed sharply of late even as overall retail sales growth remains robust. This was to be expected to some extent once we passed the one-year mark of the onset of COVID-19 in March 2020, an event that caused online sales growth to soar more than 30% over the ensuing year. Year-over-year (YOY) comparisons are much tougher for the online channel, so a growth slowdown was inevitable but is has been more acute than expected, with e-commerce retail sales growth slowing to less than 10% (YOY) in the last two quarters as more people returned to in-store shopping (Exhibit 3). That’s less than pre-pandemic growth rates for the online channel. In fact, store-based sales growth has outpaced online gains for the last two quarters (Exhibit 3), causing online market share to decline from a quarterly pandemic peak of 21% in 2Q20 to approximately 19% in 3Q21 — still well above its pre-pandemic market share of 16% in 1Q20 (Exhibit 4). (It should be noted that an online sale is any purchase transaction consummated electronically even if the merchandise is picked up in-store or curbside.) This is a normal development, as few expected online market share gains taken in 2020 to be maintained in their entirety once we were out of the house again in large numbers.

A surprising revelation involves Amazon’s 3Q21 operating results, which showed a 3.3% (YOY) increase in retail product sales, short of expectations. We estimate the retail powerhouse lost market share for the first time — approximately 150 basis points lower, leaving some to wonder if this showing was a canary in a coalmine. Amazon’s retail guidance for the holiday mentioned its determination to absorb rising costs wherever possible to win holiday sales, which is not great news for smaller retailers who cannot afford to absorb these expenses.

Fortunately, these developments likely reflect a recent shift of spending preferences back towards in-store shopping rather than an overall spending slowdown. That’s a critical point. Consumers have gotten reacquainted with in-store shopping after avoiding most indoor venues for nearly a year. We are all tired of being mostly housebound, and vaccinations have made it safe for most Americans to be out and about again. Strolling the aisles feels pretty good after such a lengthy hiatus but we don’t know how long that good feeling will last.

Our survey respondents’ attitudes towards in-store and online shopping as we near the end of COVID era living are consistent with high-level retail sales data, which tell us that in-store shopping has enjoyed a comeback in 2021 as more Americans resume some semblance of their pre- COVID lifestyles. However, store-based retailers shouldn’t rejoice prematurely. Few of our survey respondents have any intention of frequenting stores as much as they did before COVID.

Online shopping retains its mass appeal.

- Two-thirds of respondents are either shopping online as much as they did during COVID (44%) or trying to shop online as much as possible (22%).

- Twenty-one percent of respondents said they were shopping online less than during COVID but more than in pre-COVID times.

- Just 13% said they had reverted to pre-COVID online shopping habits.

- These responses are consistent with the theme that online shopping may not hold all market share gains it took in 2020 but will retain most of it.

In-Store shopping makes a comeback in 2021.

- Nearly a year since the announcement of the first COVID vaccines, 40% of respondents said they were shopping in-store as much as they were pre-COVID.

- The remaining 60% were divided into three groups: 25% said that they have shopped in-store less since the Delta variant of the COVID virus became widespread; 24% are shopping in-store more than in 2020 but less than in pre-COVID times, and 11% said they had no intention of ever shopping in-store as much as they did in pre-COVID times.

- Interestingly, these responses were highly consistent across income groups.

Make no mistake about it, we are not going back to where we were as shoppers in 2019. Online shopping has benefitted hugely since the pandemic and consumers won’t ever revert to their pre-COVID shopping ways, but some backslide was to be expected once shoppers became more comfortable with in-store shopping again. Shoppers are now in the process of deciding what their shopping habits will be in a post-pandemic world. In whatever ways consumers choose to get their shopping done once COVID-19 is completely behind us, large omnichannel retailers are best positioned to accommodate those preferences.

U.S. Online Retail Forecast Revision is Slightly More Favorable

We’ve revised our forecast for U.S. online retail sales for 2021 to $873 billion, up slightly from our mid-year forecast of $865 billion, which represents a 14.9% increase (YOY) from 2020. However, this annual rate of increase is highly frontloaded, with a 39% increase (YOY) in 1Q21, which was the last quarter to be compared to a pre-COVID quarter. The spike in COVID-related deaths in January and February 2021 — which represented peak COVID deaths nationally — contributed largely to the surge in online sales in 1Q21. Subsequent quarters in 2021 have shown YOY increases for online sales in the vicinity of 10%, as they are comping against post-COVID periods in 2020. Rates of increase for online sales going forward will mostly likely remain in this range, as the period of explosive COVID-induced growth is over.

Moreover, our upward revision to online sales in 2021 is entirely the result of stronger retail sales generally, which exceeded our expectations going into the year, rather than sizeable market share gains. Consequently, we expect online market share of retail sales to increase slightly for the year to 19.3% from 19.0% in 2020. Again, this pickup was achieved entirely in 1Q21, with online market share slipping a bit in 2Q21 and 3Q21 compared to prior year quarters as in-store sales surged once vaccination rates climbed. In short, muted market share gains for the online channel in 2021 is primarily attributable to surprisingly strong in-store sales rather than flagging online sales.

For consumers, it’s still unclear whether this renewed affair with in-store shopping is just a fling or a rekindled relationship that will endure. Like some other activities we thought we missed during the pandemic, in-store shopping has seen an initial burst of activity as we emerged from our shelters, but let’s not forget how unfavorably store traffic figures were generally trending prior to the pandemic. We’re betting that this rekindled romance will start to fizzle once the novelty of it gives way to familiarity.

Consumers’ Financial Conditions and Outlooks Vary Widely as We Look to Exit the COVID Era

It has been said that the COVID era and our nation’s response to the pandemic in all its aspects has contributed to uneven, arguably starkly different outcomes for many Americans, thereby creating distinct sets of COVID-related winners and losers that affect our perceptions of current conditions. Some responses to our consumer survey support this notion that many of us see things quite differently as we are poised to exit the COVID era. Some other noteworthy responses include the following:

Vast majority of respondents received federal stimulus payments and half of those recipients used it primarily to buy stuff.

- Nearly 80% of respondents received stimulus payments in 2021, which is consistent with most estimates on the matter.

- One-half of respondents told us they used stimulus money primarily to purchase essentials (38%) or splurge items (12%), while 22% paid down debts and 14% saved or invested this money. Another 14% said they did a bit of all these things.

- However, some responses varied notably by income group, with more lower income respondents (33%) using stimulus money to reduce debt rather than save/invest (4%).

More than one-half of respondents said their stimulus money is now mostly gone.

- Some 54% of respondents said their stimulus money was mostly gone, having used it for spending or debt reduction, while another 31% said they still had some (20%) or most (11%) of their stimulus money. The remainder (16%) said stimulus money was either saved or invested and wasn’t available for spending.

- This response indicates that some stimulus money is still available for holiday spending, with nearly one-third of respondents saying they still had at least some of it.

- By income group, 66% of lower income respondents said their stimulus money was mostly gone compared to 51% for the higher income group, who have more of their stimulus money still available.

Respondents’ personal financial condition relative to pre-COVID times varies widely.

- Thirty-one percent of respondents said their personal financial condition is worse today than it was prior to COVID-19, 30% said their financial condition is mostly unchanged, while 20% said their financial condition is slightly better, and 19% said it is much better.

- This response varied notably by income group, with 40% of lower income respondents saying their personal financial condition has worsened since COVID compared to 25% for higher income respondents.

- Just 26% of lower income respondents said their financial condition had improved to any degree since COVID-19 struck compared to 46% of higher income respondents.

Consumers are very divided on their outlooks for 2022.

- Thirty-five percent of respondents said COVID-19 will be mostly/entirely behind us in 2022, which will be a strong year for the U.S. economy.

- Thirty-four percent said COVID impacts effects will linger in 2022 and hold back the economy from full strength.

- Twenty percent said the economy will be permanently changed from COVID and will widen the divide between winners and losers.

- Eleven percent expect that COVID-related impacts will cause the economy to weaken or deteriorate in 2022 vs. 2021.

- These responses varied notably by income groups, with 42% of higher income respondents expecting a strong year in 2022 compared to 28% for the lower income group. (Exhibit 5)

Wrapping It Up

A once-in-a-lifetime viral pandemic that momentarily threatened to undermine the global economy has turned out to be a brief but severe economic downturn from which recovery began quickly. An unprecedented federal response to the pandemic contributed greatly to minimizing the financial impact and duration of the downturn, mainly by committing close to $2 trillion (with a T!) to individuals, businesses, and municipalities while the U.S. economy was finding its footing. Ironically, the COVID-19 pandemic has turned out to be a financial windfall for many U.S. households and most large retailers. Few saw that coming, as Americans redirected much of their spending during the pandemic towards consumables and home and hearth categories, which continues to this day.

E-commerce sales benefitted tremendously from the pandemic, with online market share picking up approximately 400 basis points of market share from 1Q20 to 1Q21 before relinquishing 60 basis points of market share in the last two quarters as shoppers returned to stores in greater numbers.

Retail sales have shown very impressive strength throughout 2021 and there is little reason to believe this momentum will dissipate in the homestretch of the year. However, much of the financial relief that has greased the skids for robust consumer spending has faded, and this should cause some deceleration in retail sales growth in the months ahead. Issues around supply chain bottlenecks, soaring shipping and fulfillment costs and producer price inflation will remain looming wildcards into 2022 but nobody truly knows what their ultimate impact will be on product availability or consumer demand as we close out an otherwise standout year.

It’s unlikely that these malign forces are sufficient to undermine the prospects for a merry holiday season. However, any forecasts for double-digit sales growth are ignoring or minimizing these headwinds. That said, a merely solid holiday season would more than suffice in 2021, as most large retailers chalk up another respectable year amid a most unusual time.

Related Insights

Related Information

Published

November 19, 2021

Key Contacts

Key Contacts

Senior Managing Director, Leader of Retail & Consumer Products Practice

Managing Director