Does the Corporate Debt Maturity Wall Really Exist?

-

07. Nov 2023

Herunterladen Download Article

Download Article

-

Anyone working in the restructuring profession undoubtedly has encountered the ominous term “debt maturity wall” in relevant business articles and industry publications. Much like other feared apparitions such as the Loch Ness monster and Sasquatch, the maturity wall is visible at great distance but never up close. Similarly, these sightings are episodic and the evidence of their very existence is flimsy, yet they remain fixed in the public’s mind. What keeps them going? The possibility that they are real.

The term “maturity wall” dates to 2010, in the aftermath of the global financial crisis. By that time, aggressive actions taken by global state actors and central banks helped avert the doomsday scenario of a spiraling meltdown of the global financial system, and the worst of the economic downturn was behind us. But nobody had yet signaled the all-clear. Corporate credit markets were again functioning somewhat normally after seizing up at times in late 2008 and 2009, and companies borrowed vigorously once that window finally opened. U.S. leveraged credit issuance totaled $465 billion in 2010, which exceeded the combined issuance total of $3101 billion in 2008-2009 and was respectably close to pre-crisis issuance amounts of $500+ billion annually. The domestic economy was crawling out of the cave from which it would fully emerge in 2012.

The first mention of “maturity wall” we found was in late 2010, when a Moody’s report stated, “…the pending wall of debt maturities between 2011-2014 is moving forward, and heightening issuers’ refinancing risk.”2 Within a few years the term “maturity wall” had become widely used in business vernacular, referring to the growing wall of staggered corporate debt maturities that collectively built over time as more speculative-grade companies stepped up their borrowing and methodically refinanced debt securities one or two years ahead of scheduled maturity — and assumed they could continue to roll maturing debt forward on similarly favorable terms and conditions. “Kicking the can” became a related term in restructuring circles during those years, referring to the practice of an opportunistic debt refinancing that averts a potential restructuring event, which is only possible when credit markets accommodate it. “Kicking the can” caused the “maturity wall” to grow higher.

The first year that the maturity wall was supposed to crash Corporate America was 2012. Many LBOs completed in 2007 — the final and frothiest year for buyouts prior to the financial crisis were financed with leveraged loans having five- or six-year tenors. Surely credit markets would have little appetite to refinance these loans in the aftermath of that cataclysmic episode. (Wrong!) Furthermore, banks were reluctant to declare corporate loans in default in 2008-2009 (though they could have) for reasons other than payment defaults. Springing maturities, tripped financial covenants and other technical defaults often were waived or suspended during those tenuous 18 months, while scheduled loan maturities were sometimes extended — the first appearance of the “amend & extend” (A&E) practice that prevailed for several years thereafter. Many of these A&E loans had their maturities pushed out to 2012, when it would be time to pay the piper. A Moody’s senior credit analyst said at the time, “An avalanche is brewing in 2012 and beyond if companies don’t get out in front of this.”3 They did — and most of these leveraged debt maturities were refinanced, with those maturities pushed out to 2014-2016. Leveraged credit issuance approached $675 billion in 2012, including HY bond issuance that topped $300 billion for the first time, and was followed by then-record-high issuance of $975 billion in 2013.4

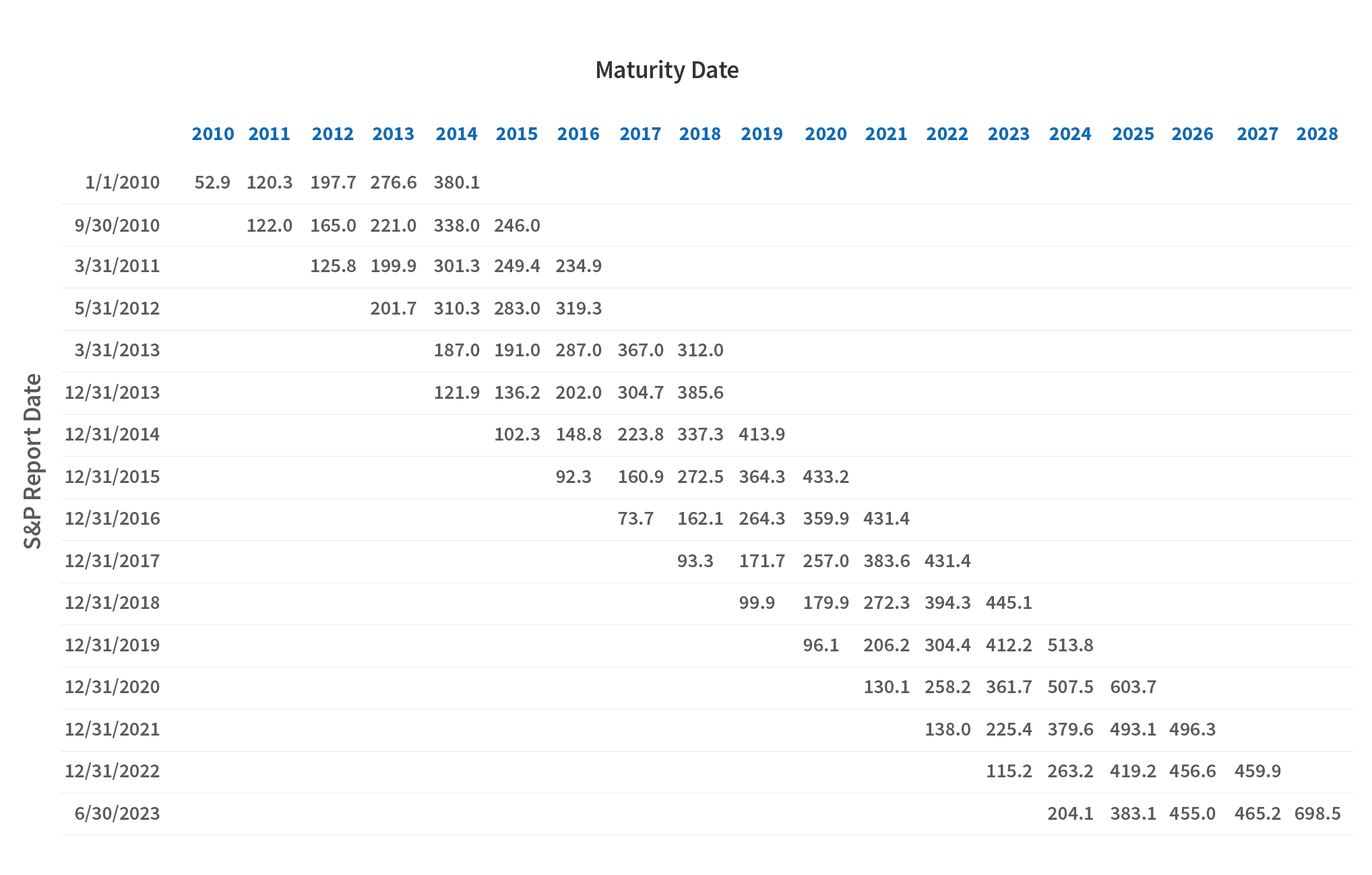

Cutting to the chase, the drama of the maturity wall has flared up in the business media every couple of years since 2012 but never with any consequence. Each time, the daunting debt maturity wall that was four to five years out was subsequently whittled down in the interim until amounts due by the time that distant year drew near became manageable, as we have exhaustively documented in Figure 1. As the maturity wall repeatedly was pushed out, the amounts due in distant years grew even larger, but again without consequence as time marched on. Today, U.S. speculative-grade debt maturities coming due in 2028 total nearly $700 billion. This is far greater than the $380 billion of scheduled 2014 debt maturities back in early 2010, though risky borrowers have grown in number, size and earnings, so we don’t want to overdramatize the absolute amount of that change. But can this game continue indefinitely?

Of course, the great enabler in repeatedly pushing out the maturity wall has been massive quantitative easing by the Fed for the better part of the last 15 years, not only during crises but also in years when the domestic economy had no obvious need for such aggressive intervention. For instance, consider that the size of the Fed’s balance sheet ballooned from $2.8 trillion to $4.5 trillion between 2012 and 2014, a larger absolute increase than Fed purchases during the global financial crisis. Since Fed asset purchases are paid for by crediting banks’ reserve accounts, this is indirect money creation. Beyond that, the “Fed put” — the belief that the Fed would use monetary easing to support financial markets, if necessary — took hold in credit markets and further encouraged risky lending and easing standards.

Today, the “Fed put” is dead, interest rates are at 16-year highs, and leveraged credit markets arguably are in their most perilous moment since 2008-2009. As we continue to see extreme liability management exercises carried out with near regularity by hard-pressed borrowers, there should be no misunderstanding about what is happening. Lenders are reaping the consequences of what they sowed for years in the form of loose or permissive provisions in credit documents negotiated with borrowers, typically large PE sponsors, which permit many of these bold maneuvers. None of this happened by neglect or happenstance. It is the inevitable result of a financial world awash in liquidity for a decade, where the bargaining advantage favored borrowers and lenders willingly capitulated to their aggressive demands or risked missing out on a deal — and perhaps future deals. The explosion of private credit in recent years only gives borrowers further negotiating leverage to press for favorable loan terms and leaky provisions that would have been inconceivable 15 years ago.

Recently (since aggressive Fed tightening began in mid-2022), the pendulum has swung back towards lenders, which has made traditional lenders more circumspect about lending standards and somewhat more demanding on terms. But as we’ve seen since early summer, companies stepped up to the plate once the borrowing window opened wider, and leveraged debt issuance — bonds and loans — has been more robust in recent months. And again, many speculative-grade debt maturities for 2024 have been addressed, except for the weakest borrowers that cannot access leveraged credit markets in this high-rate environment.

As for the implication of these developments on the maturity wall, the notion that leveraged credit markets would ever experience a major paradigm shift away from loose credit standards — a moment of clarity when they collectively would decide they won’t do all those kinds of aggressive deals anymore — seems a bit naïve in retrospect and unlikely going forward. There is just too much money dedicated to be lent, and that is no less true today than it was several years ago. In particular, the ascent of private credit (which now tops $1 trillion (AUM) and competes with the syndicated institutional lending market for large leveraged loans, but was only a nascent source of capital ten years ago) seems poised to enter its golden age, according to some industry watchers. Private credit loans topping $1 billion are no longer rare, nor are multi-billion private credit funds. That is not to say that the money spigot is wide open or that bad decisions won’t be made, but money must be deployed — that is the highest priority — and any negative consequences of that are down the road.

More likely than a paradigm shift, changes in credit market practices and risk appetites will be incremental and happening around the edges. For instance, buyouts levered at 6X EBITDA likely still will get financed, but not deals at 7X-8X EBITDA. Moreover, “higher for longer” interest rates certainly will impair the ability of some high-risk borrowers from rolling their debt, and defaults will accelerate, but it seems improbable that credit markets will find that old-time religion in the absence of a prolonged economic slump or shock event. Again, the maturity wall won’t be consequential, at least not before 2025, so let’s give it a rest for now. Like other mythical creatures, it seems that the dreaded maturity wall will remain a figment of our minds. But you never know.…

Figure 1 – Analysis of S&P Rated U.S. Corporate Speculative-Grade Debt Maturities Since 2010

Footnotes:

1: Refinitiv LPC

2: “U.S. Speculative-Grade Bank Credit Facilities Due 2011-2014: Tidal Wave of Refunding is Approaching,” Moody’s Investors Service (December 1, 2010).

3: "Junk Bond Avalanche Looms for Credit Markets,” Dealbook, The New York Times (March 16, 2010), Link.

4: Source: Refinitiv LPC. Note that leveraged credit refers to institutional term loans plus high-yield bond issuance.

Related Insights

Related Information

Datum

07. Nov 2023

Ansprechpartner

Ansprechpartner

Global Co-Leader of Corporate Finance & Restructuring