The Hidden Effects of Universal Proxy Cards

Inside the Numbers of What Really Changed

-

November 14, 2023

-

The introduction of universal proxy cards (“UPC”) for U.S. companies in September 2022 was intended to make it cheaper and more efficient for activist shareholders to run campaigns, and for shareholders to vote “a la carte” for director nominees.1, 2 As a result, some advisors predicted an increase in activist investor campaigns, as well as a higher likelihood that activists would win contests and gain more board seats.3, 4, 5 Initial results for the 2023 proxy season in the U.S. indicate that, to date, neither of those occurred. Looking at the top line numbers, this year’s proxy season initially appears similar to the last few seasons.

However, a deeper look reveals several notable differences. In the past, activists winning board seats without support from both major proxy advisors, Institutional Shareholder Services (“ISS”) and Glass Lewis, was extremely rare; this year was a different story.

Another change this season was a bit counter-intuitive. Many believed that UPC would make it easier to compare activist and company board nominees head-to-head and, thus, companies would be more proactive in refreshing their boards. However, the opposite has occurred in 2023, with fewer Russell 3000 companies adding fewer directors than in prior years.6

Activism Level Similar to Previous Years

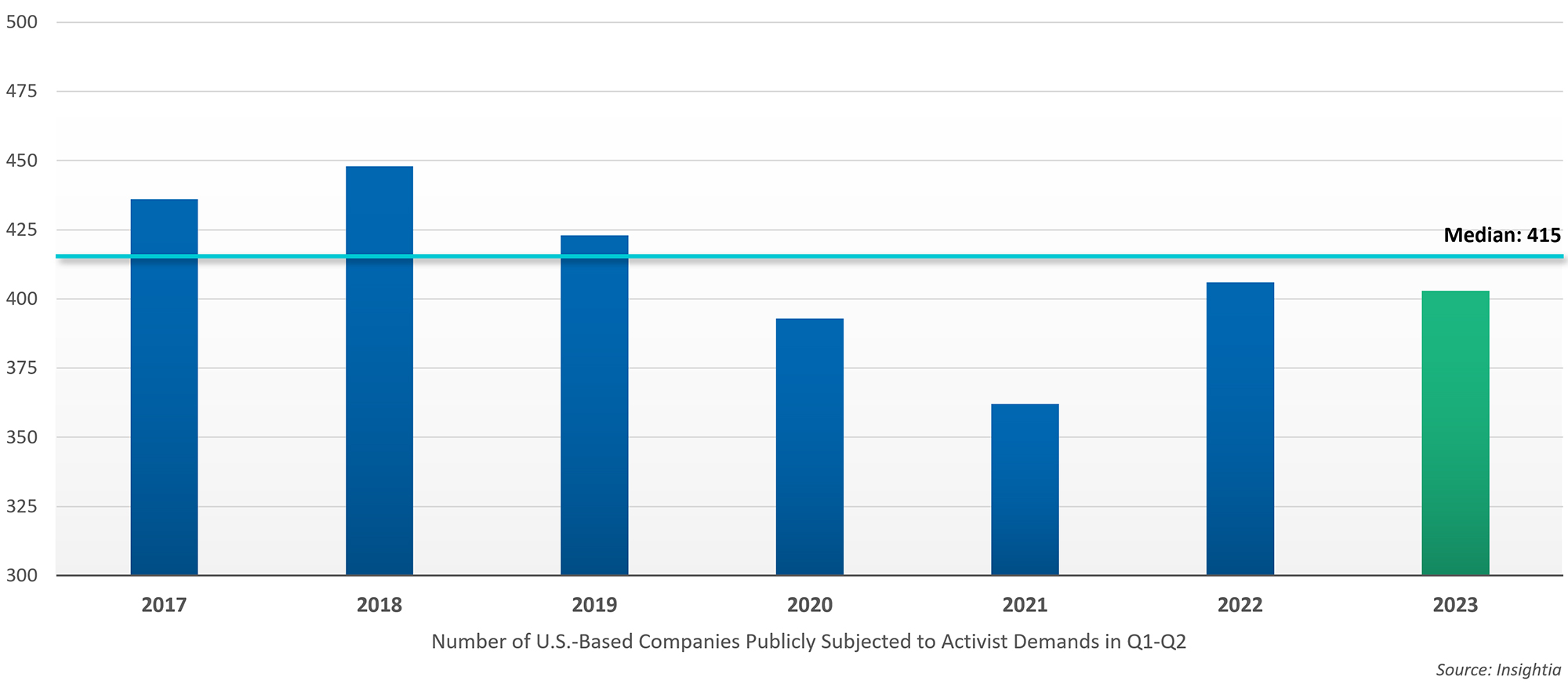

A total of 403 U.S.-based companies were publicly subjected to activist demands in the first half of 2023, according to Insightia.7 That is in line with the previous six years. The number of U.S. companies targeted during the first half of any year between 2017 and 2022 ranged from 362 to 448, with a median of 414 companies targeted.8

Figure 1: U.S. Activist Targets

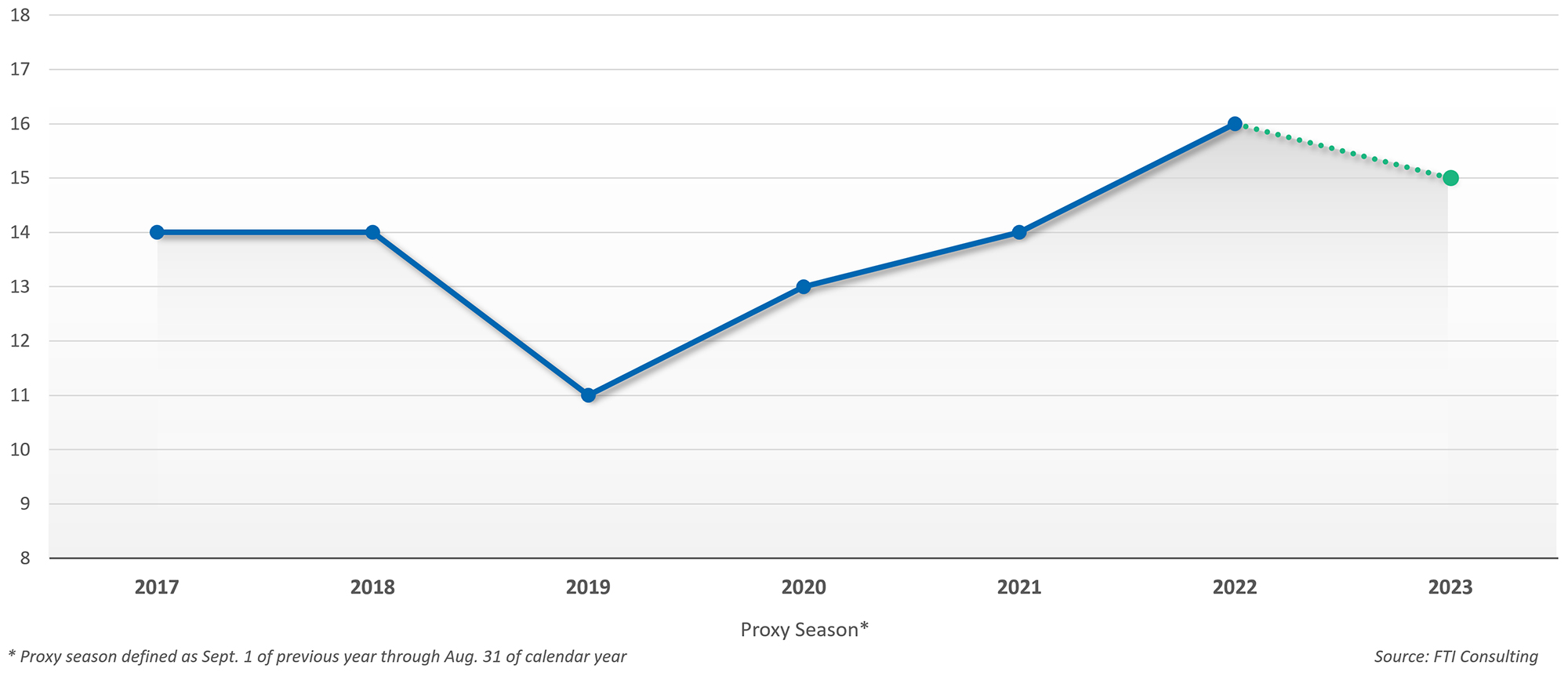

The number of full-scale proxy contests was also similar; from September 1, 2022 through August 31, 2023, there were 15 proxy contests that met the following criteria: U.S-based companies with a market capitalization of at least $100 million, where both ISS and Glass Lewis published recommendations. In each of the previous six proxy seasons, there were between 11 and 16 contests, with a median of 14 contests per season.9

Figure 2: Full Scale Proxy Contests

Activists’ Success Rates At or Below Prior Years

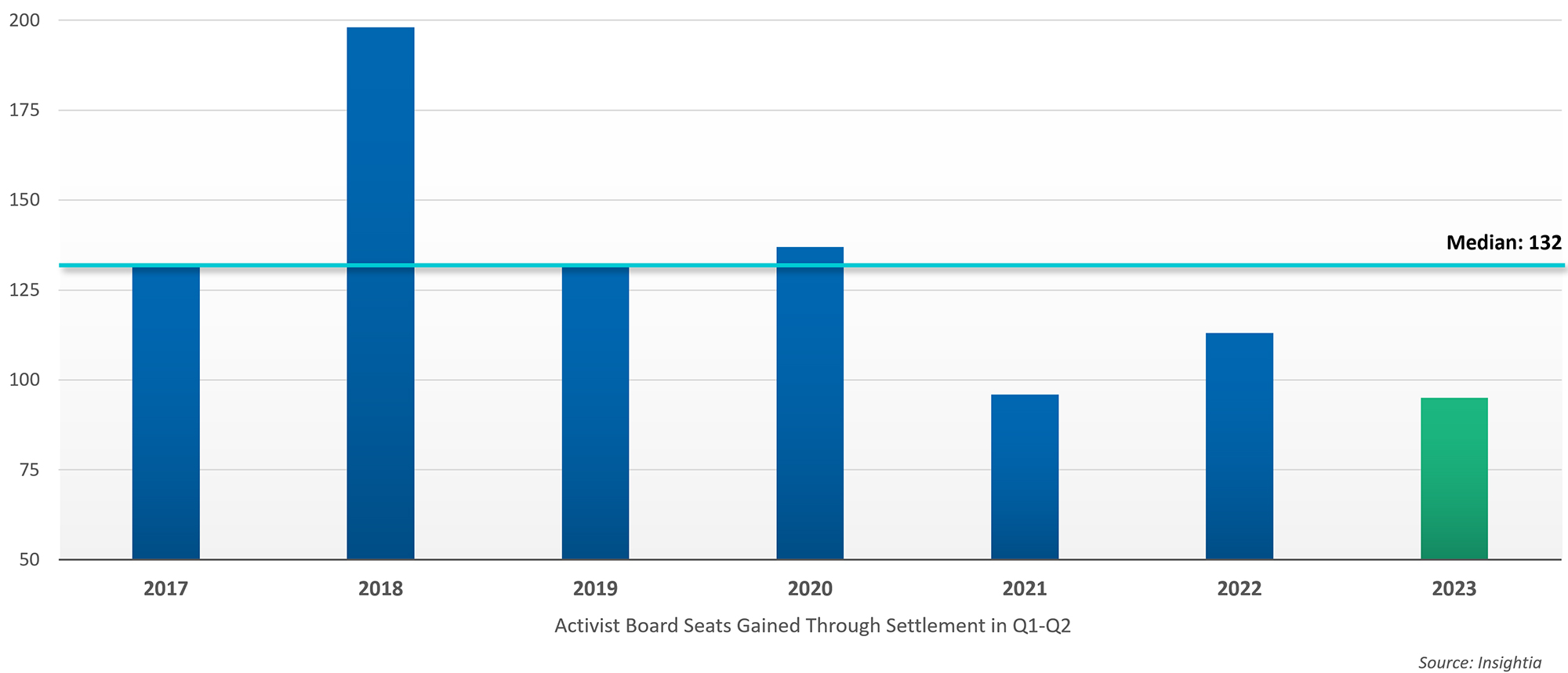

Activists have typically gained the vast majority of board seats through settlements with their targets. In the first half of 2023, the number of board seats that activists gained through settlements, and overall, were below those of previous years. For example, activists gained a total of 95 seats in 1H 2023. During the first half of each year from 2017 through 2022, activists won between 96 and 198 seats, with a median gain of 132 board seats.10, 11

Figure 3: Seats Won by Activists

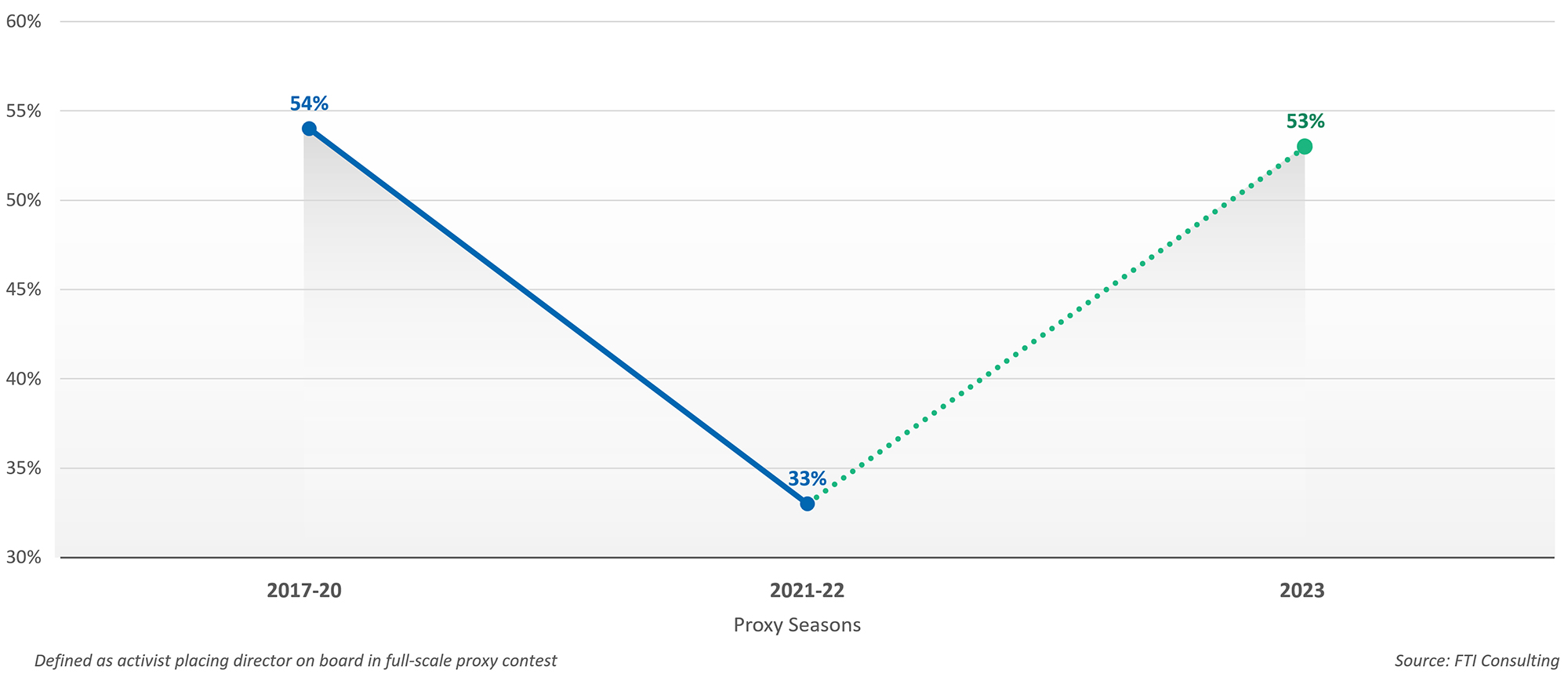

Activists’ success rates within proxy contests rebounded from low levels in the past two seasons, but were comparable to those of the 2017-2020 seasons. This season, activists won a seat 53% of the time, in eight out of 15 contests. During the 2017 through 2020 seasons, activists won at least one seat in 54% of proxy contests; in the 2021-2022 seasons, that figure fell to 33%.

Figure 4: Activists' Success Rate

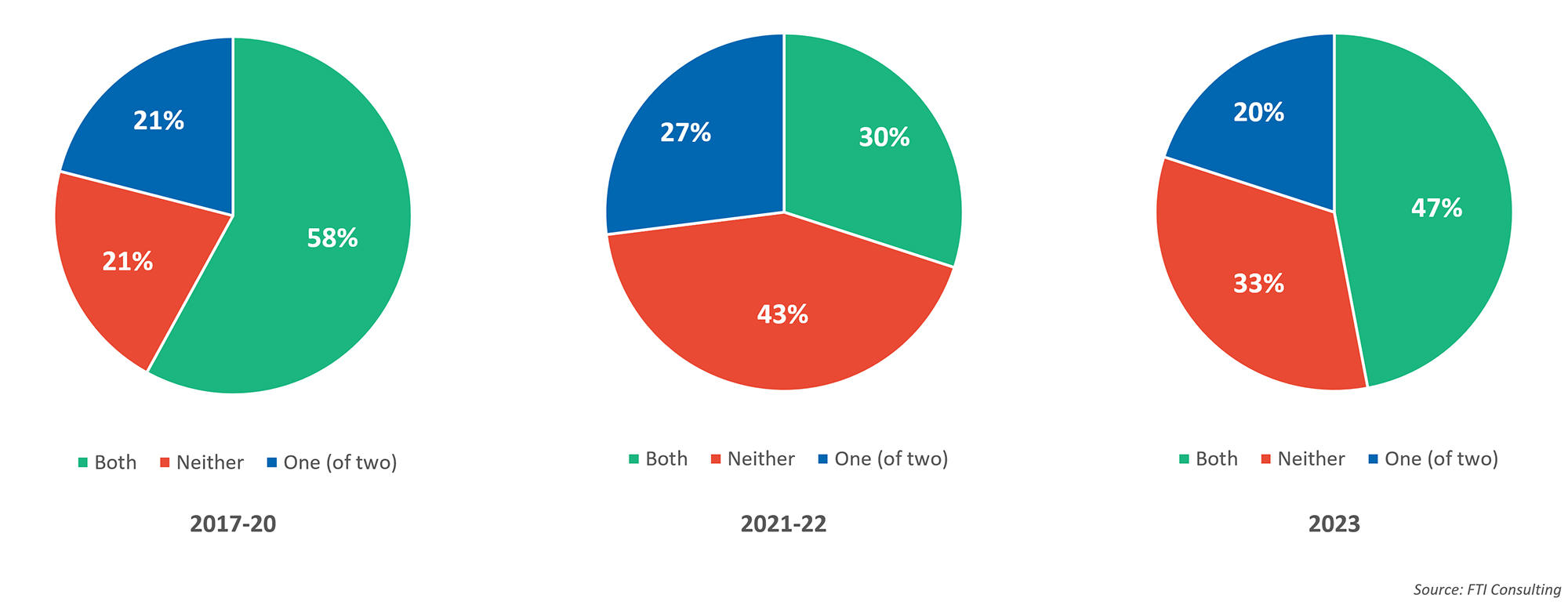

Activists’ success rates closely track the frequency with which proxy advisors recommend for them. In the 2023 season, activists gained the support of both ISS and Glass Lewis 47% of the time, compared with 58% in the 2017-2020 seasons and 30% during the 2021-2022 seasons. Activists won the support of neither proxy advisor in 33% of contests this season, as opposed to 21% in the 2017-2020 seasons and 43% during the 2021-2022 seasons.12

Figure 5: How Often ISS & Glass Lewis Recommended for Activist

ISS and Glass Lewis each stated in summer 2022 that their guidelines for evaluating proxy contests would not change with the implementation of UPC.13, 14 Their recommendations appear to confirm that proxy advisors’ criteria have remained consistent.

Naturally, proxy advisors’ support is critical, for both activists and issuers. During the 2017 through 2022 seasons, only twice in 82 contests did an activist win a board seat without the support of both major proxy advisors. No activist won a seat without support from at least one advisor.15

The results in 2023 were different. In December 2022, in the first contest under UPC to go all the way to a shareholder vote, activist Land & Buildings won one of two board seats that it sought against Apartment Investment & Management Co.16, 17 ISS recommended for one Land & Buildings nominee, while Glass Lewis recommended for the issuer.18, 19

In February 2023, Sarissa Capital Management won all seven seats it pursued versus biopharmaceutical company Amarin Corp. (“Amarin”), even though both ISS and Glass Lewis recommended for all directors nominated by Amarin.20, 21 Two months later, activist Daniel J. Mangless won all three seats he sought against Zevra Therapeutics, Inc. (“Zevra”), despite both proxy advisors recommending for Zevra’s nominees.22, 23

It is unclear exactly why shareholders favored activist nominees in these situations, but Amarin and Zevra each had large retail shareholder bases and had underperformed the Russell 2000 Biotechnology Index by at least 60 percentage points over the five years ended December 31, 2022.24, 25

Fewer New Directors Than in Previous Years

UPC requires both sides in a proxy contest to list all director nominees.26 This allows shareholders greater ability to choose the precise combination of directors that they want. Having all nominees listed on either card also lets shareholders more easily compare nominees head-to-head. It is more likely than in the past that an activist could nominate someone perceived as a far better candidate than an incumbent director, and then persuade shareholders to elect its nominee on that basis alone, without making the strong case for change at the company which is typically required to win a contest. As such, just one vulnerable director on a company’s board could incentivize an activist to run a campaign.

Companies can begin to address this concern by conducting an analysis of the strengths and weaknesses of their board as a whole, of the directors who sit on it, and what their skills and backgrounds add. In many cases, a fulsome examination may lead a company to refresh its board, with a focus on specific skill sets and experience where the company found its board deficient. In doing so, the company could replace one or more weaker or long-tenured directors with directors likely to be viewed as better qualified, by both shareholders and proxy advisors.

These types of self-evaluations can and should happen behind closed doors. It is possible that companies are performing these evaluations more often than in the past. However, the available data suggests otherwise.

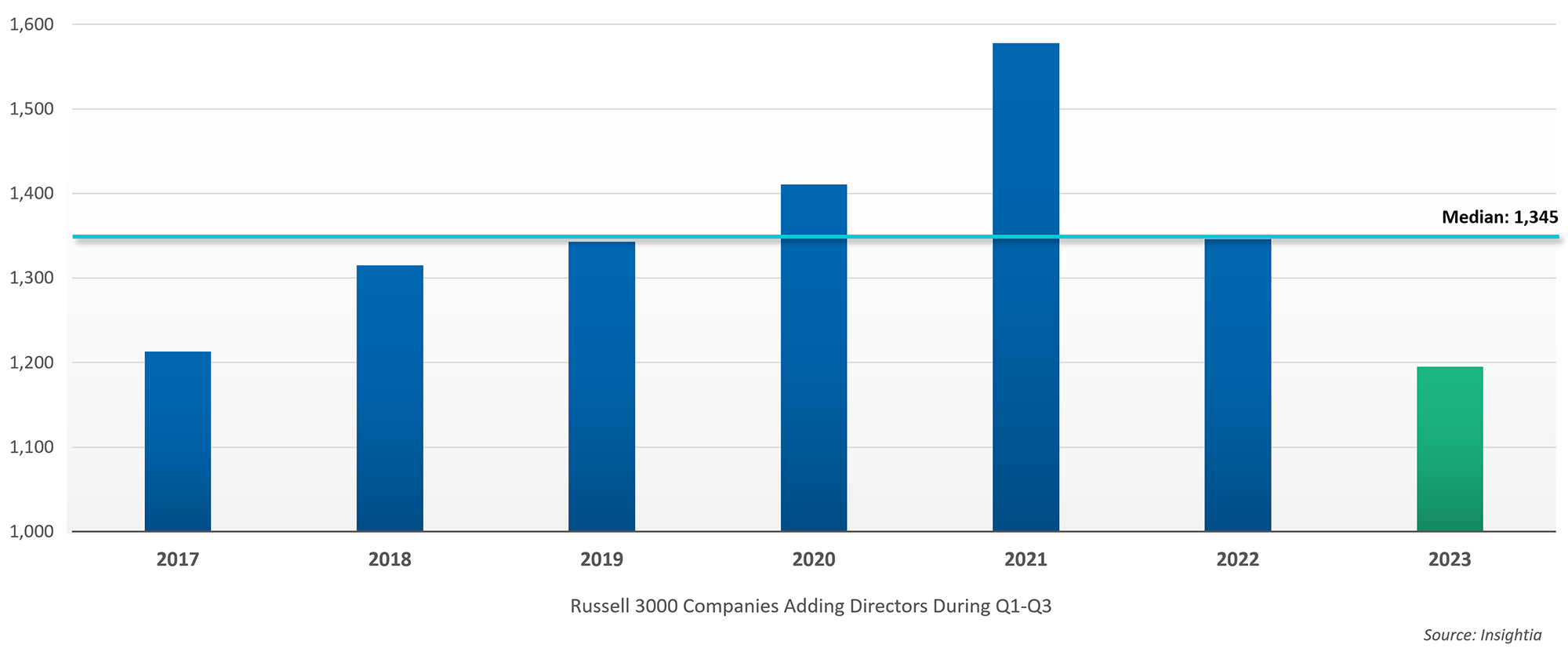

According to Insightia, during the first nine months of 2023 (Q1-Q3), 1,195 companies in the Russell 3000 added directors. That was fewer companies adding directors than in the first nine months of any of the previous six years. During each of those prior periods, at least 1,213 Russell 3000 companies added directors, with a median of 1,345 companies adding directors.27

Figure 6: Companies Adding Directors

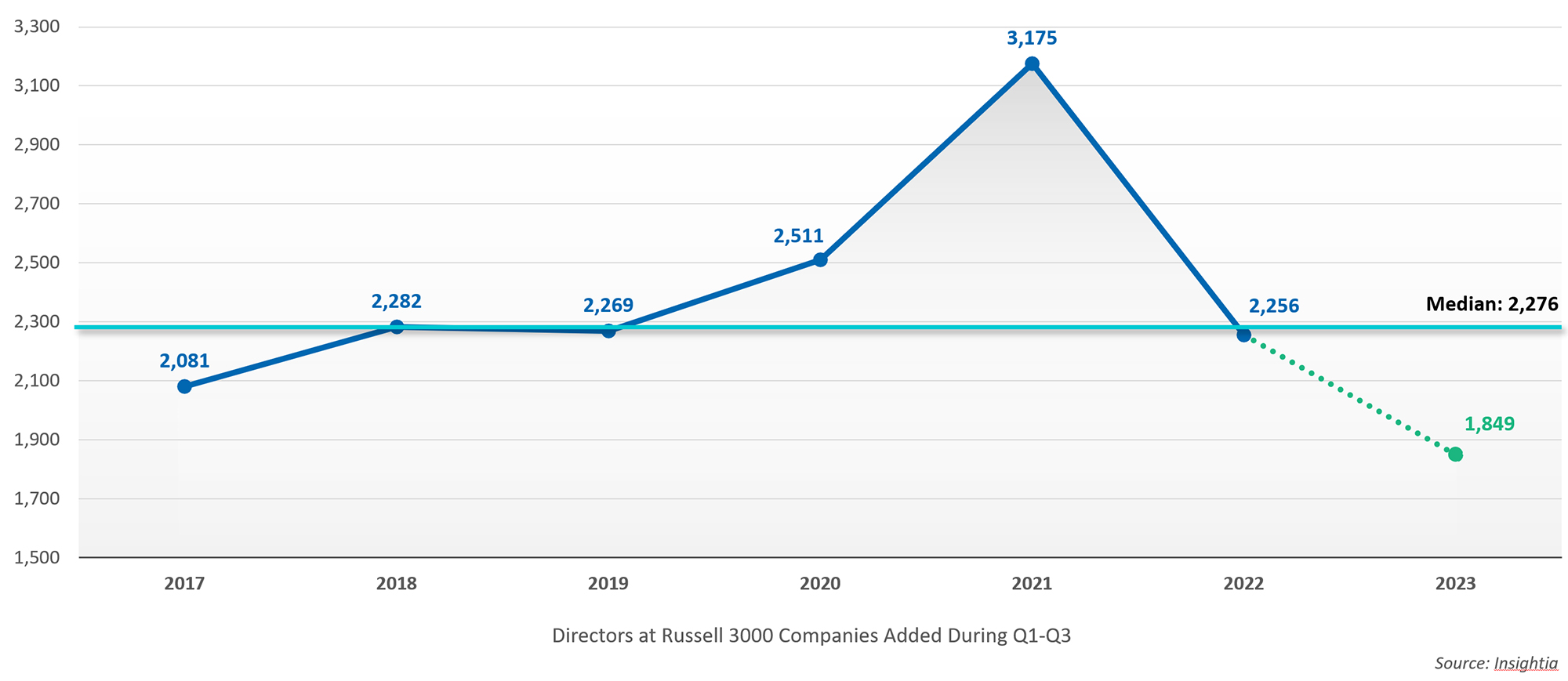

Similarly, Russell 3000 companies appointed fewer directors in Q1-Q3 23 than in any corresponding period from 2017 through 2022. This year, 1,849 directors were appointed, below the previous low of 2,081 appointed in Q1-Q3 17, and well below the median of 2,276 appointments in the first nine months of each year from 2017 through 2022.28 Taken together, these data points indicate that companies have not accelerated their board refreshment cycle, despite the heightened risk that UPC brings.

Figure 7: Directors Added

Conclusion

Slower turnover among public company directors is not something that would have been expected during the first year of UPC. The success that activists had in several proxy contests, where they did not earn the support of both ISS and Glass Lewis, may also be surprising. The combination of these factors may embolden activists to more frequently target companies with perceived weak directors. These developments should further encourage companies to review their directors’ skillsets for the current marketplace and to evaluate potential board refreshment on an annual basis.

Footnotes:

1: Michael Levin, “The Cost of Proxy Contests,” Harvard Law School Forum on Corporate Governance, (May 25, 2022)

2: Ronald Oral, “Activist Investing Today: Goodwin’s Sean Donahue on Universal Proxy Cards and More,” The Deal, (June 23, 2022)

3: Kai Liekefett, Derek Zaba, and Leonard Wood, “Welcoming the Universal Proxy,” Harvard Law School Forum on Corporate Governance, August 8, 2022

4: Lauren Thomas, “Companies Brace for Onslaught of New Activists After Change in Proxy-Voting Rules,” Wall Street Journal, Nov. 20, 2022,

5: Louis L. Goldberg, William H. Aaronson, and Ning Chiu, “Practical takeaways of universal proxy card,” Harvard Law School Forum on Corporate Governance, Nov. 9, 2022

6: Insightia database of Russell 3000 director appointments and exits.

7: Insightia, Shareholder Activism in H1 2023, published July 19, 2023

8: Ibid.

9: FTI Consulting defines a “season” as from September 1 of the previous year through August 31 of that year.

10: Insightia, Shareholder Activism in H1 2023, published July 2023.

11: Insightia, Shareholder Activism in H1 2020, published July 2020.

12: Based on research conducted by FTI Consulting.

13: Sidley update, “ISS Provides Guidance on the Universal Proxy Card, Puts ‘Weakest’ Directors on Notice,” Aug. 24, 2022

14: Mark Grothe, “The Implementation and Implications of Universal Proxy Cards,” Glass Lewis, Sept, 1, 2022

15: Based on research conducted by FTI Consulting.

16: “Aimco Announces Preliminary Voting Results of 2022 Annual Meeting of Stockholders”, Aimco, Dec. 16, 2022

17: “ISS Recommends Aimco Shareholders Vote for Change on Land & Buildings’ Blue Universal Proxy Card,” Business Wire, Dec. 5, 2022

18: Ibid.

19: “Leading Proxy Advisory Firm Glass Lewis Recommends that Aimco Stockholders Vote ‘FOR’ Aimco’s Three Highly Qualified Director Nominees,” Business Wire, Dec. 1, 2022

20: “Sarissa Capital Wins Proxy Contest Against Amarin by Huge Landslide,” Business Wire, Feb. 28, 2023.

21: “LEADING INDEPENDENT PROXY FIRM ISS JOINS GLASS LEWIS IN RECOMMENDING THAT AMARIN SHAREHOLDERS VOTE “AGAINST” SARISSA’S VALUE-DESTRUCTIVE PROPOSALS,” Amarin, Feb. 16, 2023

22: “Honigman Advises Daniel Mangless in Successful Board Nomination for Zevra Therapeutics,” Honigman, April 27, 2023

23: “Leading Proxy Advisory Firms ISS And Glass Lewis Demonstrate Strong Support For Zevra’s Transformation Strategy,” Zevra, April 17, 2023

24: Source: FactSet share price performance.

25: Ibid.

26: Mark Grothe, “The Implementation and Implications of Universal Proxy Cards,” Glass Lewis Sept. 1, 2022

27: Source: Insightia database of Russell 3000 director appointments and exits.

28: Ibid.

Related Insights

Related Information

Published

November 14, 2023

Key Contacts

Key Contacts

Managing Director