Inflation Is Raging, Rates Are Rising and Markets Are Reeling. Where Are All the Insolvencies?

-

December 12, 2022

Downloads Download Article

Download Article

-

It has been a tough few years of fire, drought, flood and the pandemic. With increasing inflation and rising interest rates, Australians are struggling to pay their household bills and mortgages and many are facing the perfect storm of financial insecurity.

For the 35% of Australian households with a home loan,1 mortgage repayments – their single-biggest expense – have already surged by at least 40% and look set to jump higher.2 For the 30% of households that rent3 – many of whom have relatively low income and wealth – rent has increased by about 10% in the last year.4 Higher rents could push some renters into financial stress, particularly when combined with broader cost-of-living pressures.

Over the 12 months to the September 2022 quarter, the CPI rose 7.3%,5 and the situation is unlikely to improve any time soon. For example, spiking grocery inflation is expected to be sustained over the next few months due to the ongoing floods and as rising supply costs are passed through to prices in supermarkets.6

Together, these factors have reduced consumer confidence. In early December, the ANZ-Roy Morgan Consumer Confidence metric came in 26.6pts below the same week a year ago and 47% of Australians said their families were worse off financially than this time last year.7 Despite strong Black Friday retail sales, 45% of Australians say now is a “bad time to buy” major household items.8

No Respite in Sight

The state of the current geopolitical situation suggests none of these pressures are likely to improve in the near term. The war in Ukraine is now in its tenth month,9 with no visible end in sight to the hostilities and little prospect that the disruptive global economic impacts of the war will dissipate anytime soon. As a result, the war’s wider effects on the global economy have become entrenched. Most global commodity prices are off their multi-year peaks of early March but remain very elevated and will likely remain higher for longer than anyone previously imagined. High commodity prices benefit Australian exporters but do have a flow on effect to domestic producers in areas such as gas prices. Putting it all together, any scenario of a short conflict in Ukraine with a limited and transitory global economic impact seems less likely with each passing day.

Although some economists believe Australia may still avoid a recession,10 growth is slowing due to the measures that are used to curb inflation starting to bite. U.S. inflation appears to be reaching its peak, but still may not be tamed by year-end as several factors contributing to global price spikes have intractable causes beyond the control or influence of government policymakers and central banks, who can only hope to slow demand via rate hikes and monetary contraction. Caught in the slipstream, Australia will continue to fight rising inflation for months to come. The Reserve Bank forecasts that inflation will peak at around 8% by the end of 2022 before gradually moving back to the top of the target band of 3% by the end of 2024.11

Where Are All the Insolvencies?

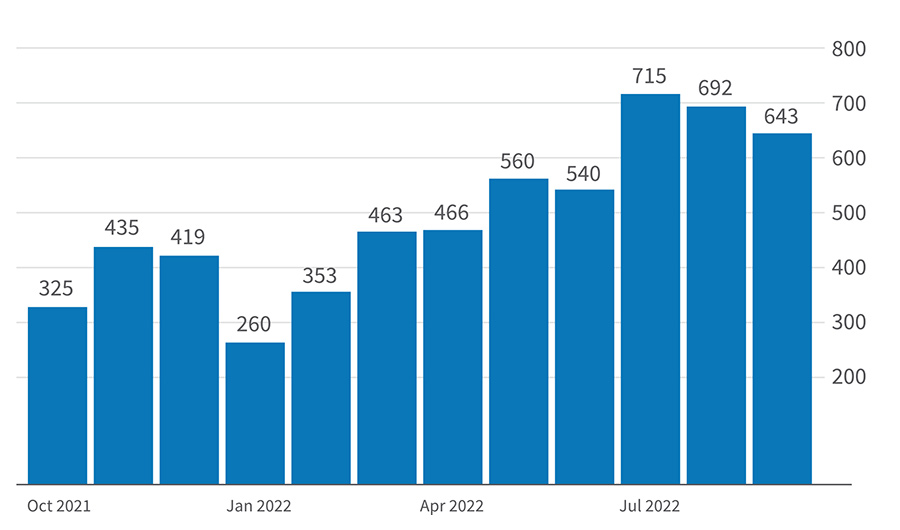

Given a weakening economic backdrop, and the end of pandemic-era support, it seems inevitable that corporate insolvencies will begin to rise. This appeared to be happening in July, when ASIC data showed 715 firms had entered into external administration in July – the highest level since November 2019.12 This was more than double the lows of 2020 and 2021, when policies like JobKeeper and temporary changes to insolvent trading laws kept potential corporate failures afloat. However, since July, the figures have started heading downwards. External administrations in Australia fell to 692 companies in August and then again to 643 companies in September 2022 (Exhibit 1).

Exhibit 1 - Source: ASIC13

Why is this happening? The obvious but unsatisfying answer is that it’s just too soon to expect an appreciable upturn in insolvencies. History says there is normally a time lag of six to nine months between changes in the economic climate and their impact on restructuring activity. We aren’t quite there yet. However, that explanation is becoming a bit tiresome and, perhaps, less persuasive as the year progresses.

The most plausible explanation for still-muted restructuring activity is closely tied to leveraged credit market conditions that prevailed in 2020-2021. During this window, higher-risk issuers were able to borrow huge sums at low rates with few strings attached in the way of performance-based maintenance covenants and fewer restrictions on access to and uses of capital (and, often, underlying collateral), giving them financial runway and flexibility to withstand adverse business conditions for an extended period without consequence until liquidity is exhausted, if it comes to that. The list of troubled issuers that undoubtedly would have restructured by now were it not for opportunistic credit market rescues or forbearance by lenders has grown lengthy, and many continue to confront challenges in fixing their businesses.

Traditional safeguards in credit documents that have given lenders or other debtholders the ability to intervene in a troubled credit long before the money runs out often have been weakened or negotiated away by borrowers in recent years. This trend has been in place for a while but now seems like standard practice in leveraged lending circles. Moreover, in those instances when financial covenants have been tripped or events of technical default have occurred since COVID struck, many lenders have been reluctant to exercise their full rights and remedies and are more inclined to grant a waiver, amend credit documents and collect a fee. That tendency remains in place even after COVID-related business impacts have faded. These developments can either postpone or avert a restructuring event, depending on what companies are able to accomplish with this breathing room.

Will highly leveraged borrowers have sufficient liquidity to ride out whatever adversity comes their way in the next year? In Australia, soaring costs and a Tax Office crackdown on unpaid debts may dictate otherwise. If insolvencies surge, the worst casualties are likely to be in the construction and manufacturing sectors. Construction saw the largest increase in administrations over the past year, due to supply shortages and extreme upticks in material costs.14 Manufacturing sector administrations also increased sharply in July, with east coast manufacturers hit by sky-rocketing natural gas prices.15

Of course, that all depends on the severity and duration of that adversity – and nobody has a clear read on that currently, with forecasts of growth, earnings and inflation being all over the place. We are in uncharted waters today, and nobody should have strong convictions about where the global or Australian economies will be a year from now.

Our experienced team is skilled at engineering and executing formal and informal solutions to maximise value from distressed or insolvent companies. Whether it’s providing an in-depth turnaround plan to drive value in a restructure, or supporting clients in more distressed situations on how to move forward with a sale or exiting the business.

Our senior leaders and qualified liquidators can accept formal appointments across Australia and can swiftly mobilise a team on the ground to respond to the urgent needs of a client. They combine an unprecedented depth of knowledge and experience across regions, geographies and technical capabilities – tailored to the situations and challenges facing a business. Our primary focus is always to provide the best outcome possible for stakeholders.

We are also accustomed to dealing with the practical issues that are the difference between success and disaster.

Footnotes:

1: “Housing: Census - Information on housing type and housing costs,” Australian Bureau of Statistics (last visited 7 December 2022), https://www.abs.gov.au/statistics/people/housing/housing-census/2021.

2: Amy Remeikis, “Up to a third of mortgage holders could struggle to keep up with repayments, RBA says,” The Guardian (19 July 2022), https://www.theguardian.com/australia-news/2022/jul/19/mortgage-holders-could-face-large-jump-in-repayments-if-interest-rates-reach-3-rba-says.

3: “Housing: Census - Information on housing type and housing costs,” Australian Bureau of Statistics (last visited 7 December 2022), https://www.abs.gov.au/statistics/people/housing/housing-census/2021.

4: Niko Iliakis, “What is the average rent in Australia in 2022?,” Mozo (6 October 2022), https://mozo.com.au/home-loans/articles/what-is-the-average-rent-in-australia#:~:text=Whether%20you%27re%20looking%20at.

5: “Consumer Price Index, Australia,” Australian Bureau of Statistics (last visited 7 December 2022), https://www.abs.gov.au/statistics/economy/price-indexes-and-inflation/consumer-price-index-australia/latest-release.

6: “Widespread floods will force inflation above 8 per cent for fruit and vegetables, treasurer says,” ABC News (21 October 2022), https://www.abc.net.au/news/2022-10-21/fruit-and-veggies-price-hike-inflation-floods/101562114.

7: “ANZ-Roy Morgan Consumer Confidence virtually unchanged at 82.7 to start December,” Roy Morgan (last visited 7 December 2022), https://www.roymorgan.com/findings/9125-anz-roy-morgan-consumer-confidence-december-6.

8: Ibid.

9: Tucker Reals, Alex Sundby, “Russia’s war in Ukraine: How it came to this,” CBS News (23 March 2022), https://www.cbsnews.com/news/ukraine-news-russia-war-how-we-got-here/.

10: Peter Hannam, “Australia predicted to avoid worst of downturn as IMF warns of global recession,” The Guardian (12 October 2022), https://www.theguardian.com/business/2022/oct/12/revenue-boost-will-aid-budget-repair-as-storm-clouds-loom-over-economy-deloitte-predicts#:~:text=The%20 consultancy%20expects%20Australia%20will,growth%20slows%20and%20inflation%20rises.&text=%E2%80%9CAustralia%20is%20in%20a%20slightly,at%20Deloitte%2C%20 told%20Guardian%20Australia..

11: “Statement by Philip Lowe, Governor: Monetary Policy Decision,” Reserve Bank of Australia (6 December 2022), https://www.rba.gov.au/media-releases/2022/mr-22-41.html. 12 Australia Bankruptcies: Bankruptcies in Australia decreased to 643 Companies in September from 692 Companies in August of 2022,” Trading Economics (last visited 7 December 2022), https://tradingeconomics.com/australia/bankruptcies#:~:text=Bankruptcies%20in%20Australia%20averaged%20644.79.

13: Ibid.

14: “Financial Stability Review – October 2022 - Box C: Financial Stress and Contagion Risks in the Residential Construction Industry,” Reserve Bank of Australia (last visited 7 December 2022), https://www.rba.gov.au/publications/fsr/2022/oct/box-c-financial-stress-and-contagion-risks-in-the-residential-construction-industry.html.

15: Michael Read, “Bankruptcy laws to be reviewed amid jump in business failures,” Financial Review (28 September 2022), https://www.afr.com/politics/bankruptcy-laws-to-be-reviewed-amid-jump-in-business-failures-20220928-p5bljg.

Published

December 12, 2022

Key Contacts

Key Contacts

Senior Managing Director, Head of Australia Corporate Finance & Restructuring