National Property Sector Overviews: Mid-Year 2023

-

05. Sep 2023

Herunterladen Download Article

Download Article

-

Industry market participants are closely monitoring the commercial real estate (CRE) market, which has been affected by macroeconomic uncertainty and continuing fears of a potential recession as well as the residual effects of the COVID work from home (WFH) phenomenon. Since the Federal Reserve (Fed) started raising rates in early 2022 to curb inflation, the CRE investment market has been affected by increased lending costs, and uncertainty as to when and where interest rates will peak and the pricing of assets impacted by WFH. Tight monetary policy raised the cost of borrowing and reduced liquidity. Commercial property price index data from providers such as Green Street, MSCI and NCREIF1 show property valuations generally declining in all sectors except for the hotel sector, leading to greater industrywide concern and challenges. There are challenges ahead for owners faced with a refinancing in the next 18 to 24 months with significantly higher interest rates and only modest growth in income, or worse - declining income. Some landlords are making a proactive decision that a property is obsolete and not worth the debt considering the cost to update or repurpose the asset.

Based on FTI Consulting’s research, we present overall real estate sector highlights and a more detailed discussion for each of the four core property types (office, industrial, multi-family apartment and retail) plus hotel below:

Overall

- CRE investment activity will remain constrained for all sectors, given tight CRE lending standards and high interest rates.

- Distress transactions will increase as loans mature in a challenging and expensive borrowing environment, creating opportunity for well-capitalized and patient investors.

- Capital market volatility will recede as inflation decreases and interest rates stabilize and begin to decline, signaling it is safe again to transact.

- CMBS performance will continue being challenged by high interest rates and uncertainty in the CRE market.

- Environmental, social and governance (ESG) in CRE will continue to be an investor focus to prioritize an asset’s appeal to attract credit-worthy tenants.

- Flight to quality persists as investors pursue properties with enhanced building amenities and proximity to public transportation.

- High construction costs combined with high interest rates continue to stall or cancel projects.

- Higher operating costs continue to erode margins for both owners and tenants.

- The Association of Foreign Investors’ Real Estate Q1 2023 International Investor Survey2 indicated that the United States is still regarded as a preferred destination for CRE investment.

Office Market

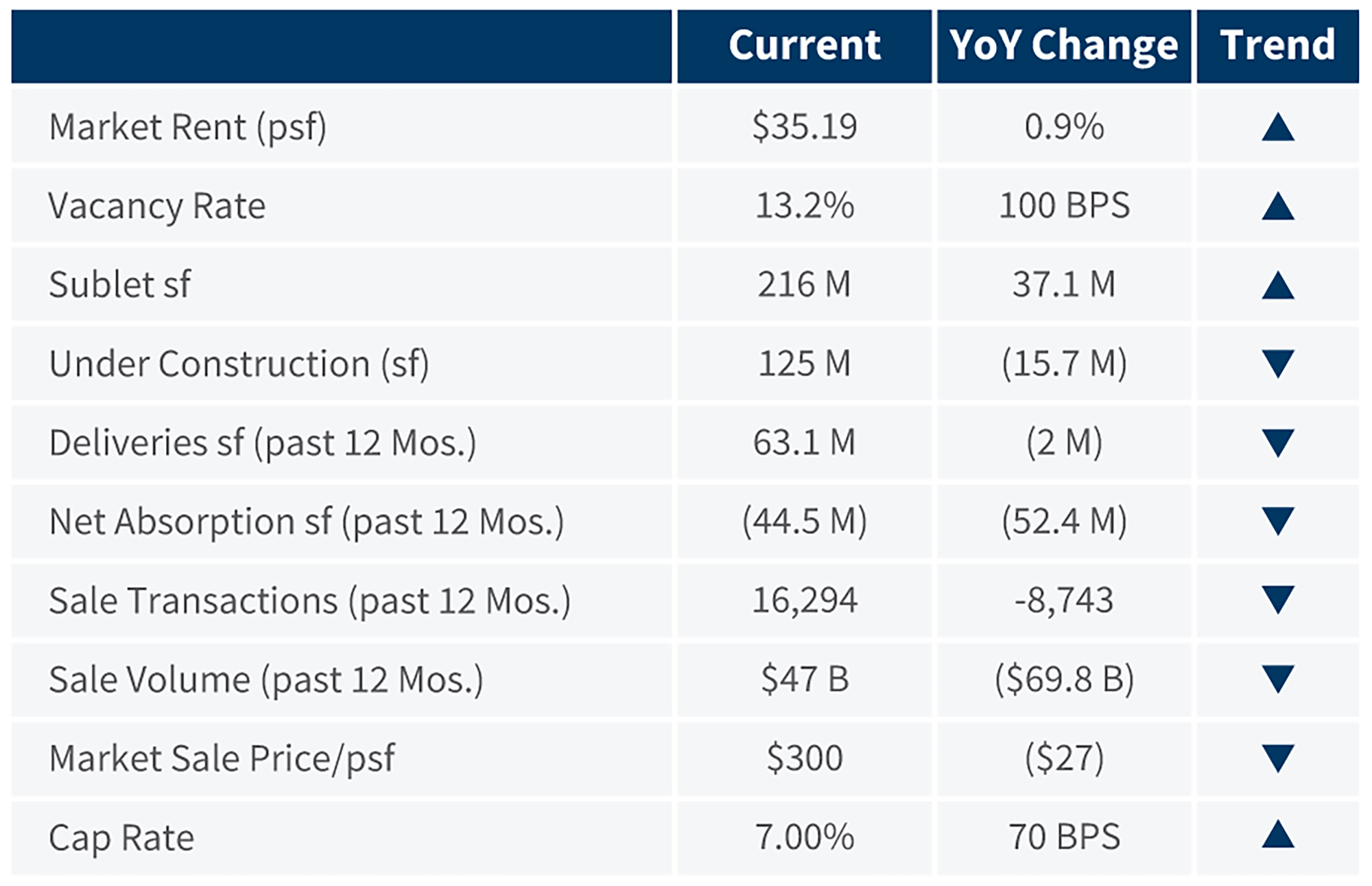

- Vacancy exceeds highs of the Great Recession due to declining space demand.

- Sublet space has increased 120% since the end of 2019 and 21% YoY to a record level.

- Net absorption was negative for the fifth consecutive quarter in 2023 with the pace of vacant spaces accelerating.

- Rent growth is generally flat with more sublet space on the market.

- Slowing construction did not positively impact vacancy.

- Investment sales activity during the first half of 2023 was the lowest since 2010.

National Office Market Indicators

Source: Data compiled from CoStar (as of July 11, 2023).

Below are key metrics for the largest office markets in the United States:

10 Largest Office Markets (by Inventory) Comparison

Source: Data compiled from CoStar Industrial National Report - United States (July 11, 2023).

Note: 12 Mos. represents August 2022 to July 2023 period.

Source: Data compiled from CoStar Industrial National Report - United States (July 11, 2023).

Source: Data compiled from CoStar Industrial Capital Markets Report - United States (July 11, 2023).

Note: 12 Mos. represents August 2022 to July 2023 period.

Insights:

Office market recovery faces many challenges.

- Hybrid work models continue being implemented by firms.

- Downward pressure on effective rents will persist from tenants gaining more bargaining power.

- Office utilization continues to significantly lag pre-pandemic levels per Kastle Systems’ Back to Work Barometer.3

- Market bifurcation will create more pressure to upgrade older spaces.

- Net operating income (NOI) and net absorption will continue being negatively impacted by lower renewal rates and reduced tenant footprints.

- Near-term lease expirations will continue to challenge property owners.

Industrial Market

- Market performance is cooling but steady rental rate growth and positive net absorption continue.

- Vacancy rates have increased from record lows but are still nearly 70 bps below the 10-year average.

- Inventory is set to increase 3.0% in 2023, the fastest pace of supply growth in more than three decades.

- The pace of rental gains has moderated.

- Absorption is being negatively impacted by distribution center closures from retailers reassessing logistical operations.4

- Sales volume has noticeably declined after peaking in 2022.

National Industrial Market Indicators

Source: Data compiled from CoStar (as of July 11, 2023).

Below are key metrics for the largest industrial markets in the United States:

10 Largest Industrial Markets (by Inventory) Comparison

Source: Data compiled from CoStar Industrial National Report - United States (July 11, 2023).

Note: 12 Mos. represents August 2022 to July 2023 period.

Source: Data compiled from CoStar Industrial National Report - United States (July 11, 2023).

Source: Data compiled from CoStar Industrial Capital Markets Report - United States (July 11, 2023).

Note: 12 Mos. represents August 2022 to July 2023 period.

Insights:

- Significant space deliveries in the near term are likely to increase vacancy rates in select markets.

- Current construction pipeline is still insufficient to satisfy distribution space shortages in many major coastal markets.

- Slower construction starts may result in declining vacancies and faster rent growth by mid-2024.

- Amazon began easing expansion plans in late 2022 and has reportedly closed, cancelled or delayed work on 115 U.S. warehouses in the past year, perhaps signaling moderating demand.5

- Onshoring of high-tech manufacturing is expected to drive long-term industrial demand resulting from the 2022 passage of the CHIPS and Science Act and the Inflation Reduction Act.6

- Sales volume is expected to rebound due to perceived sector safety, rent and NOI growth.

Multi-Family Market

- New supply outpaced demand during 2023 for the seventh consecutive quarter.

- Rental growth decelerated from the nearly 4.0% YoY pace at the end of 2022.

- Vacancy rates are trending near 6.0% for affordable units versus 9.0% for higher-end units.

- New construction deliveries are estimated to reach a 40-year high in 2023.

- Sales volume continues to surpass the other property sectors despite declining from the prior 12-month period.

National Multi-Family Market Indicators

Source: Data compiled from CoStar (as of July 11, 2023).

Below are key metrics for the largest multi-family markets in the United States:

10 Largest Multi-Family Markets (by Inventory) Comparison

Source: Data compiled from CoStar Multi-Family National Report - United States (July 11, 2023).

Note: 12 Mos. represents August 2022 to July 2023 period.

Source: Data compiled from CoStar Multi-Family National Report - United States (July 11, 2023).

Source: Data compiled from CoStar Multi-Family Capital Markets Report - United States (July 11, 2023).

Note: 12 Mos. represents August 2022 to July 2023 period.

Insights:

- Affordability issues will continue to pressure owners of newer luxury properties.

- Greater concessions are expected from a record new supply, resulting in higher vacancy rates.

- High housing prices, constrained supply and high mortgage rates will keep potential buyers in rentals.

- Limited investor upside is expected in the near term due to lower rent growth from elevated deliveries.

- Sector outlook remains favorable, driven by lifestyle flexibility, household growth from Generation Z and millennials, and downsizing baby boomers.

Retail Market

- Vacancy rates have declined to record lows, owing in part to minimal new construction.

- The tenth consecutive quarter of positive net absorption in 2023 resulted from steady leasing and lower move-outs.

- Most new construction consists of single-tenant, build-to-suit projects in areas with favorable demographics.

- Demolitions continue removing obsolete product from the market.

- Healthy asking rent growth continues despite moderating.

- Foot traffic at U.S. retail businesses declined 2.3% YoY in May 2023.7

National Retail Market Indicators

Source: Data compiled from CoStar (as of July 11, 2023).

Below are key metrics for the largest retail markets in the United States:

10 Largest Retail Markets (by Inventory) Comparison

Source: Data compiled from CoStar Retail National Report - United States (July 11, 2023).

Note: 12 Mos. represents August 2022 to July 2023 period.

Source: Data compiled from CoStar Retail National Report - United States (July 11, 2023).

Source: Data compiled from CoStar Retail Capital Markets Report - United States (July 11, 2023).

Note: 12 Mos. represents August 2022 to July 2023 period.

Insights:

- Retail sales grew for the third consecutive month in June 2023.8

- Consumer confidence increased to a 17-month high in June 2023.9

- Grocery-anchored neighborhood centers and single-tenant net lease assets in well-located areas continue being the most coveted by investors.

- Retail centers in secondary and tertiary markets will be challenged by limited demand and rental growth.

- More notable retailers have filed for Chapter 11 in 2023 as the supply of physical stores continues to outweigh shopper demand (i.e., Bed Bath & Beyond, Party City, Tuesday Morning, Christmas Tree Shops, David’s Bridal, Rockport Group).10

- Repositioning of underperforming assets will continue transforming the shopping experience.

Hotel Market

- The three key metrics (occupancy, ADR and RevPAR) grew during the past year from pent-up demand.

- Occupancy is still below pre-pandemic levels despite a recovery in hotel revenues.

- Rooms under construction have declined from a pre-pandemic peak of 210,000 rooms.

- Limited-service hotels comprise most projects in the development pipeline.

- Sales volume declined to the lowest first half number since 2020.

National Hotel Market Indicators

Source: Data compiled from CoStar (as of July 11, 2023).

Below are key metrics for the largest hotel markets in the United States:

10 Largest Hotel Markets (by Inventory) Comparison

Source: Data compiled from CoStar Hospitality National Report - United States (July 11, 2023).

Note: 12 Mos. represents August 2022 to July 2023 period.

Of Note: CoStar U.S. Hospitality report does not include the Las Vegas Market.

Source: Data compiled from CoStar Hospitality National Report - United States (July 11, 2023).

Source: Data compiled from CoStar Hospitality Capital Markets Report - United States (July 11, 2023).

Note: 12 Mos. represents August 2022 to July 2023 period.

Of Note: CoStar U.S. Hospitality report does not include the Las Vegas Market.

Insights:

- Steady leisure and business travel activity is projected to benefit U.S. hotels.11

- Hotel brands will continue being challenged by higher labor costs and labor shortages.12

- New development is projected to be constrained in the near term due to higher construction and debt costs.

- Domestic hotel occupancy from international travelers may increase due to a weakening dollar.13

- More focus on environmental sustainability, smart technology and unique user experiences will continue transforming the hotel experience.14

1: Commercial Property Prices Down Another 0.8%, Green Street, July 7, 2023; MSCI RCA CPPI US Commercial Property Price Indexes, May 2023; Institutional Property Values Continue Quarterly Decline, NCREIF, April 25, 2023.

2: AFIRE International Investor Survey Q1 2023 Pulse Report, underwritten by Holland Partner Group, AFIRE.org.

3: https://www.kastle.com/safety-wellness/getting-america-back-to-work/.

4: Young, Liz, Retailers are Shrinking Logistics Operations in a Changing Consumer Market, Wall Street Journal, June 5, 2023. Stroh, Kelly, Big Lots Shutters Forward Distribution Centers to Curb Costs, Excess Capacity, supplychaindive.com, June 6, 2023.

5: Young, Liz, Retailers are Shrinking Logistics Operations in a Changing Consumer Market, Wall Street Journal, June 5, 2023.

6: Lee & Associates Q1 2023 Market Reports - Industrial Overview, PDF Page 3.

7: U.S. Retailer Foot Traffic Analysis, Colliers, May 2023.

8: Smart, Tim, Retail Sales Rise Slightly in June, but Below Forecasts, usnews.com, July 18, 2023.

9: Mutikani, Lucia, US Consumer Confidence Races to 17-Month High, Housing Market Regaining Strength, Reuters, June 27, 2023.

10: Christiansen, Alex, High Profile Bankruptcies in 2023 Give a Hint to the Health of the Retail Market, La Voce di New York, July 6, 2023.

11: U.S. Travel Association, New Travel Forecast Shows Normalizing of Leisure Travel Demand from Post-Pandemic Surge, June 14, 2023.

12: American Hotel & Lodging Association, “82% of Surveyed Hotels Report Staffing Shortages,” June 5, 2023.

13: U.S. Dollar Slips Toward 15-Month Low, Euro Scales 17-Month Peak, The Business Times, July 18, 2023.

14: Hollander, Jordan, 100 Hotel Trends You Need to Watch in 2023 & Beyond, Hotel Tech Report, March 4, 2023.

Related Insights

Related Information

Datum

05. Sep 2023