The Year is Almost Over But the Party Will Continue

-

07. Dez 2023

Herunterladen Download Article

Download Article

-

“What party?” you might ask in response to this deliberately vague headline. In fact, there are several parties going strong at the moment. There’s a party raging in U.S. equity markets, fueled by the fervent belief that a soft-landing scenario will prevail, that inflation has been tamed and that the Fed’s tightening cycle is over despite repeated cautionary comments from Federal Reserve officials that none of these outcomes is yet evident or certain, with equity markets moving way ahead of the facts.

Major U.S. equity market indexes are closing the year on a bender and are within visible distance of all-time highs set in the free money-fueled rally of 2021 despite today’s stubbornly high interest rates, stalling earnings growth, and mounting economic and geopolitical challenges on multiple fronts. There’s also a kegger kicking off in leveraged credit markets, with issuance volumes picking up considerably from dismal activity levels in 1H23, and new CLOs and private credit funds being minted weekly in response to irresistible market yields for lenders that portend more robust lending activity in the months ahead. Finally, there’s a yearlong party still going strong in restructuring markets, with large Chapter 11 filings set to have their best year since 2009 aside from the pandemic-stricken year of 2020. That’s the party we’ve been circulating at in 2023, and nobody is leaving as the midnight hour of the year approaches.

The notion that financial markets are rallying fiercely while bankruptcies and other types of restructuring activity remain elevated may seem incongruous to astute observers. Moreover, the increasing diversion of corporate cash flow to debt servicing won’t abate much in 2024 if a “higher for longer” environment prevails for interest rates, meaning that incidents of business failure should remain robust well into next year. It is worth mentioning that three-month Term SOFR, the base rate for most leveraged loans, has barely budged from its cyclical high even as Treasury note yields fell by 60 bps in November. Leveraged credit markets are receptive to new issuance, and spreads have backed off from their highs of 2023, but the cost of borrowing remains prohibitively high for many “deep junk” issuers, those rated B- or worse. Many market observers are wary that recent rallies in financial markets can carry on much longer without a booze run of some sort.

Restructuring 2023: Barn Burner or Backyard Barbeque?

Despite the surge in restructuring activity, recent articles in industry publications indicate there is some debate within our circles about just how rip-roaring this year has been. Nobody disputes that it has been a very busy year for the restructuring community, but the sentiment that it has been a blockbuster is not unanimously shared. This debate is a matter of degree; some view the year as a healthy rebound from a lackluster 2022 but nothing necessarily memorable for advisory work, while others say it has been a ka-ching year, albeit one that hasn’t fit the pattern of a traditional default cycle.

Further confounding the matter, new financial advisory (FA) mandates through 3Q23 compiled by Debtwire1 have not kept pace with the increase in filing activity this year, and total FA mandates for 2023 will be within the range of average annual mandates in 2016-2019 despite considerably more filings this year, surely leaving some advisors feeling shortchanged. (Not us!)

Filings and Other Restructuring Activity Are Sharply Higher in 2023 But Aren’t Accelerating

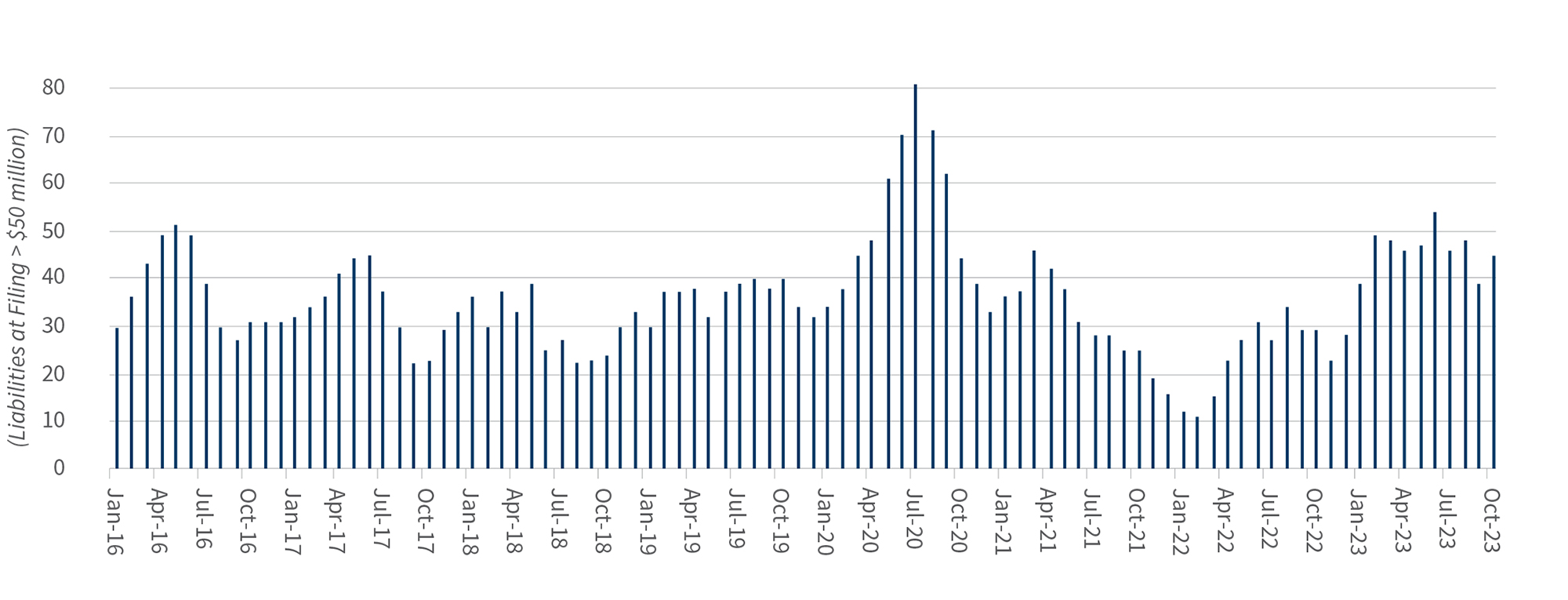

Large (>$50 million) Chapter 11 filings were strong out of the gate in 2023 and have stayed that way for most months of the year, sticking close to an average of 15 monthly filings, or nearly 185 on an annualized basis. This is well above the average annual total of 130 filings since 2010 and far above last year’s paltry total of 103 filings, but short of the 210 filings in 2020 and 255 filings in 2009. Chapter 11 filings at midyear were tracking to reach 200 filings for the year but will come up about 10% short of that mark, so there has been a slight slowing of filings in the second half.

Despite the banner year for restructuring activity by the numbers, monthly filings have not accelerated in 2023 (Figure 1) even as the effects of QT policies and economic slowing take hold. This may leave some with the impression that restructuring activity is stuck or stalling; it may be, but at quite elevated levels. The lack of upward momentum or acceleration in filings, especially in the second-half, may have tempered the enthusiasm of restructuring professionals accustomed to a crescendo of filing activity in previous cycles. If filing activity stays near current monthly levels for another year (perhaps the other “higher for longer”) — a reasonable expectation given the economic backdrop going into 2024 — any such disappointment soon will be forgotten. Unlike the mountain silhouette outlined by previous default cycles, this one will more closely resemble the mesas of the desert Southwest. In other words, what this cycle lacks in intensity, it could make up for in duration.

Some have suggested that the average size of a large Chapter 11 filing has been smaller since 2022. But our analysis indicates that the distribution of filings by debtor size in 2023 is consistent with annual averages since 2017, except for 2020, which was an outlier. Approximately 55% of large filers have liabilities at filing between $50 million and $250 million (middle-market cases); about 25% have liabilities at filing between $250 million and $1 billion (large middle-market cases), while nearly 20% of filings are above $1 billion — and 2023 was unexceptional in this respect.

Figure 1 - 3-Month Rolling Chapter 11 Filings Since 2016

Source: The Deal and FTI Consulting analysis

The Speculative-Grade Default Rate Remains Merely Average

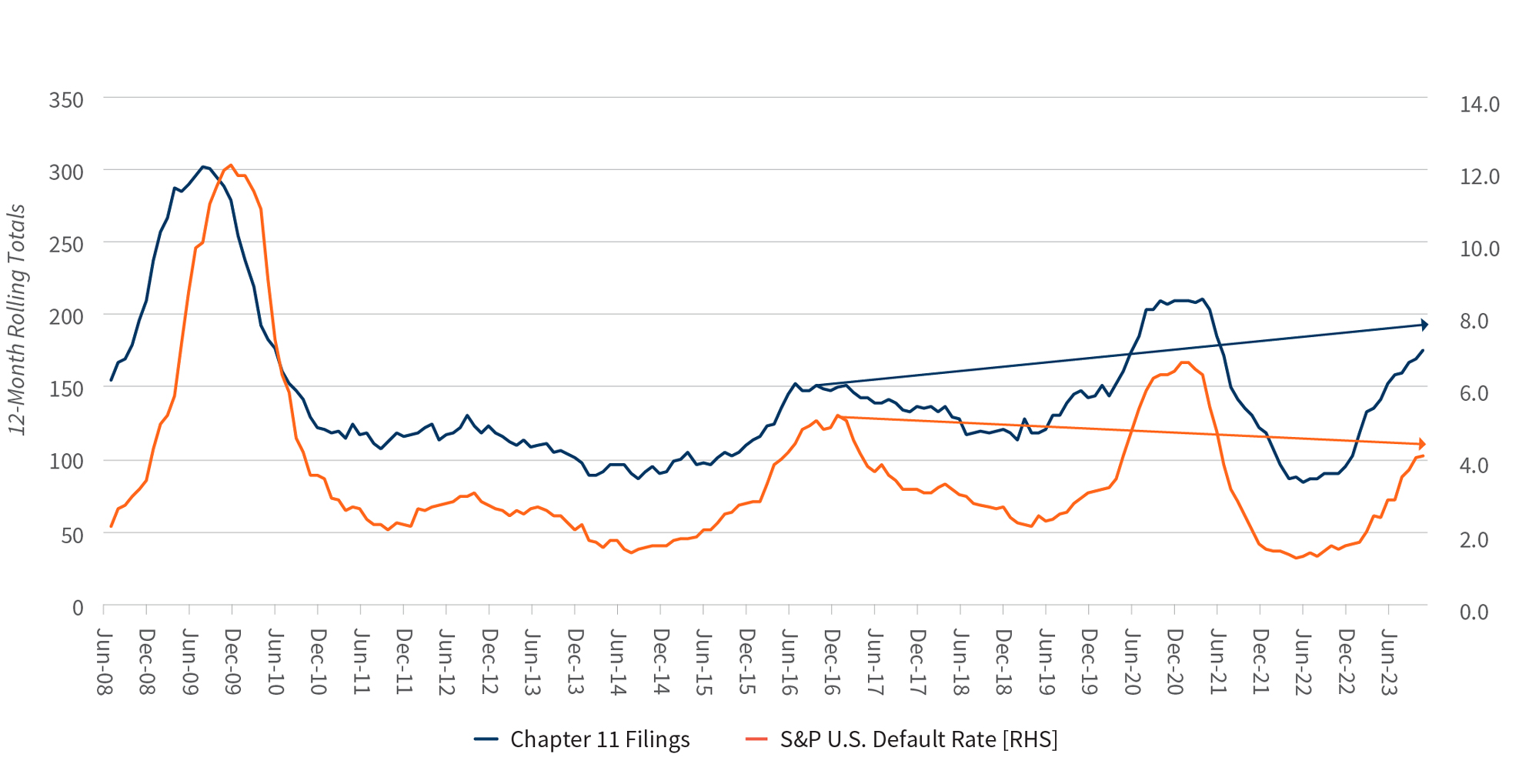

Another wet rag on an otherwise upbeat year for restructurings is the uninspired speculative-grade default rate. Despite the surge in Chapter 11 filings this year, the U.S. S&P-rated debt default rate remains close to its long-term average of 4.0%; that is, it is not yet reflective of an impending default cycle. The rate is trending higher — having doubled from near-record lows in 2022 — but remains subdued relative to any previous default cycle. While Chapter 11 filing totals in 2023 have already surpassed totals of the “mini default cycle” of 2016, S&P’s U.S. speculative-grade default rate and underlying tally of default events will come up short of that year despite more than doubling compared to 2022 (Figure 2), as restructuring activity in 2016 was dominated by large energy bankruptcies, many with rated debt.

We have mentioned previously that there is considerable overlap and strong directional correlation between the default rate and Chapter 11 filings (since a bankruptcy filing by a rated issuer is considered a default event), but they do not move in lockstep; certain corporate actions other than a bankruptcy filing, such as a distressed debt exchange, are considered default events, while many middle-market corporate borrowers do not have rated debt and therefore would not be counted in the default rate calculation should they file for bankruptcy. Rarely if ever do these two metrics of restructuring activity drift far apart, but they can meander away from each other for stretches of time.

Furthermore, the ascent of private credit likely is having some indirect impact on the default rate, as more non-bank lenders opt for credit estimates (or less) and forgo a full credit evaluation process by the rating agencies for some of their loan exposures, thereby excluding these companies from the pool of issuers tracked by the rating agencies should they later default. Consequently, we believe that, in time, the speculative-grade debt default rate could become a less representative proxy of large corporate failure, if it isn’t happening already.

S&P’s most recent base-case default rate forecast has the U.S. speculative-grade default rate hitting 5.0% by September 2024 from 4.1% currently, hardly a surge of defaults but still indicative of default activity levels in 2024 comparable to this year’s. (Note: The default rate is computed on an LTM basis, so it can move higher even as the number of monthly defaults in the year ahead stay close to recent totals, as weak default totals in 4Q22 fall out of the calculation of the default rate.)

Figure 2 - Large Chapter 11 Fillings vs. S&P Default Rate

Source: The Deal and S&P Global Ratings

Lastly, the distressed debt ratio (the percentage of speculative-grade debt issues trading at market yields indicative of financial distress) also remains subdued heading into 2024, meaning that credit markets aren’t anticipating a surge of default activity in the months ahead, though that market sentiment can change quickly.

Keep Your Party Hats On

For Corporate America, this is hardly a panic moment but for the restructuring profession it reflects a reasonable expectation of another solid year for Chapter 11 filings and debt defaults comparable to 2023 or slightly better, which most restructuring professionals would be content with. Recall that the boom-bust nature of previous default cycles has not always served our profession well in all respects.

A fertile ground for restructuring activity in 2024 will be companies that have completed reverse-merger transactions (a.k.a. de-SPACs) within the last few years. Many of these companies are generating operating losses and running low on liquidity, and are badly missing aggressive financial projections. Twenty companies that completed de-SPAC transactions since 2019 have filed for bankruptcy or liquidated in the past year, most prominently WeWork, Lordstown Motors and Cyxtera Technologies. Plenty more are coming next year, with another 80 de-SPACed companies sporting market prices of less than $1.00 per share and 90% trading below their IPO prices.2 Many of these busts won’t be headline grabbers, as most de-SPACs tend to be middle- market companies without rated debt, but they will be respectably sized restructuring transactions nonetheless.

Overall, the current moment may not be reminiscent of previous restructuring cycles, but we’d rather be at the grownup party that quietly goes until the wee hours than at the frat house kegger that runs out of beer and fizzles out by midnight.

Footnotes:

1: “Restructuring Advisory Mandates - Northam,” ION Analytics/Debtwire (September 2023).

2: Stuart Gleichenhaus and John Yozzo, “SPACs Flame Out in SPACtacular Fashion. Was It Inevitable?,” ABI Journal (December 2023).

Related Insights

Related Information

Datum

07. Dez 2023

Ansprechpartner

Ansprechpartner

Global Co-Leader of Corporate Finance & Restructuring